|

|

|

|||||||||

|

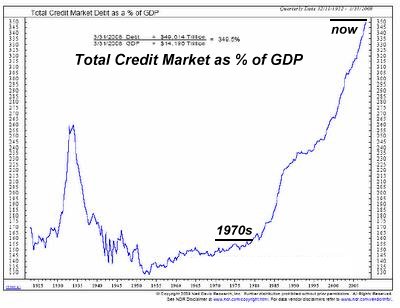

Are We Heading for a Decade of 1970s-Style Stagflation? (April 7, 2010) Four key factors in the 1970s were very different from present conditions, and that argues against 1970s-style stagflation as a model fpr 2010-2020. Sometimes history rhymes--but only for the first line. On the surface, there are reasons to anticipate a 1970s-style stagflation in the decade ahead: a stagnating economy beset by rising inflation. Four fundamental factors that profoundly influenced the economy in the 1970-1980 period are not present today. As a result, we must be careful not to expect history to rhyme stanza after stanza. 1. Demographics: the Baby Boom came of age and started households en masse. Baby Boomers bought houses, cars, furniture, etc. for their new households, and started businesses which created even more demand. In other words, the demographic macro-environment was one of strongly rising demand for goods, services and credit. Housing leaped not just in response to inflation but in response to strong organic demand from 78 million Baby Boomers. The demographic trend is now reversed; the Boomers are saving money for retirement and shedding assets to fund their healthcare and the costs of no longer being productive (retired). Governments are having to channel huge sums from spending into their pension funds for retiring Boomers. (Disclosure: I am 56 and thus a Boomer, and I do not expect to draw a dime of Social Security or Medicare.) 2. Imports were limited, giving domestic suppliers pricing power (the ability to pass on higher costs to consumers). It is rarely noted that the U.S. emerged from World War II with little competition as many of its global manufacturing competitors lay in ruins. While Japan and Germany began exporting autos to the U.S. in the 60s, it wasn't until later in the 70s that Japanese goods offered serious pricing competition to domestic producers (anyone remember the Datsun B210?). This allowed domestic producers to pass rising input and labor costs to consumers, feeding the inflationary cycle. Now many of the manufactured goods sold in the U.S. are made elsewhere, and the competitive environment is fierce; the only firms with pricing power are those with technologically "hot" goods like iPhones. 3. The quadrupling of oil prices rippled through the economy, raising costs for everything. Energy is a cost input to virtually every good and service, and the price jump of 1973 spread higher costs throughout the economy. As this raised prices, it was inflationary, and as it was in effect a new tax on the economy, it lowered demand and spending, causing stagnation. In response to that 1970s increase in oil costs, the U.S. economy became more efficient in its use of petroleum, i.e. the amount of oil consumed to generate every dollar of GDP has fallen. The big unknown in the decade ahead is the timing of Peak Oil, that is, when global supply falls irrevocably below baseline demand. As I have stated here many times, I believe we are in the "head-fake" stage when global Depression (oops, "Great Recession") is cutting demand so much that there is still enough surplus production to keep prices relatively low. As the output from supergiant fields falls, then all this surplus production will at best be replacing supply lost to depletion. When Peak Oil kicks in, then $300/barrel will seem like a "fair price" and the shockwave to the U.S. economy will outstrip the 70s oil price shock by an order of magnitude because the low-hanging fruit of efficiencies have been picked. But nobody knows when supply will fall irrevocably below demand, as geopolitics and physical supply are both causal factors. 4. Debt loads were low. The forced savings of the domestic workforce and Armed Forces during the War created a stupendous reserve of capital to fund new production capacity in the 1950s and 60s. Consumer debt was modest by today's standards, as was the Federal deficit. The nation reeled in shock when the Federal deficit hit a staggering $46 billion in the mid-70s --roughly $175 billion in today's dollars--a mere 11.6% of this year's $1.5 trillion Federal deficit.

So the debt load of the nation is much higher than in the 1970s, both private and public debt. More of the national income must be diverted to service that debt, depressing demand. New private borrowing is constrained by stagnant incomes and declining asset values. Higher taxes levied to fund unprecedented Federal deficit spending also reduces private demand and borrowing. In other words, we won't be able to "borrow our way" out of asset deflation and gin up a "wealth effect" as occurred in the 1980s. With three of the four conditions being reversed from the 1970s and the cost of oil in the decade ahead a big unknown, this suggests that the stagflation of that decade is not a good predictive model for the coming decade.

A special thank-you to Kevin D. and Jennifer M. for buying 10 copies of

Survival+ from me to distribute to friends and colleagues.

DailyJava.net

is now open for aggregating our collective intelligence.

Of Two Minds is now available via Kindle:

Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2010 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||