|

|

|

||||||||||||

|

The Federal Reserve's Nuclear Option: A One-Way Street to Oblivion

(February 5, 2014)

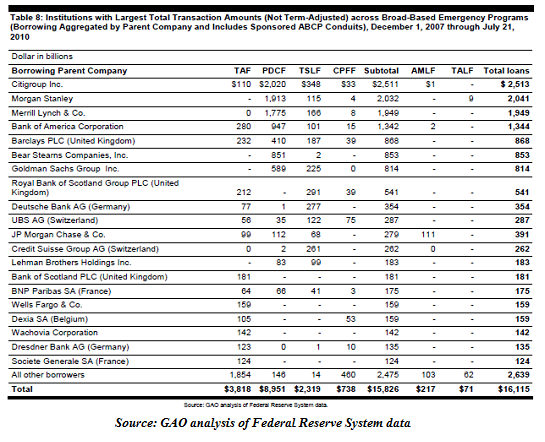

The Fed cannot create a bid in bidless markets that lasts beyond its own buying. We all know the Federal Reserve (and every other central bank) has one last Doomsday weapon to stop a meltdown in the global financial markets: creating trillions of dollars out of thin air and using the cash to buy assets that are in free-fall. This is known as "the nuclear option"--the direct monetizing of stocks, Treasury bonds, commercial real estate mortgages, student loans, corporate bonds, non-U.S. sovereign bonds, subprime auto loans, defaulted bat guano securities, offshore loans denominated in quatloos--you name it: The Fed could print money and buy, buy, buy to create and maintain a bid in bidless markets. The idea is to stop a cascade of panic by buying assets in quantities large enough to staunch the avalanche of selling. The strategy is based on one key assumption: that no more than a small percentage of the asset class will change hands in any day or week. Thus a low-volume sell-off in the $20 trillion U.S. equity markets can be stopped with large index buy orders in the neighborhood of $10 - $100 million--a tiny sliver of the total market value. But in a real meltdown, popguns will no longer conjure a bid in suddenly bidless markets, and the Fed will have to become the bidder of last resort on a massive scale in multiple markets. We need to differentiate between loans, backstops and guarantees issued by the Fed and actual purchase of impaired assets. After poring over all the data, the Levy Institute came up with a total of $29 trillion in Fed and Federal bailout-the-financial-sector loans and programs. The GAO found the Fed alone issued $16 trillion in loans and backstops:

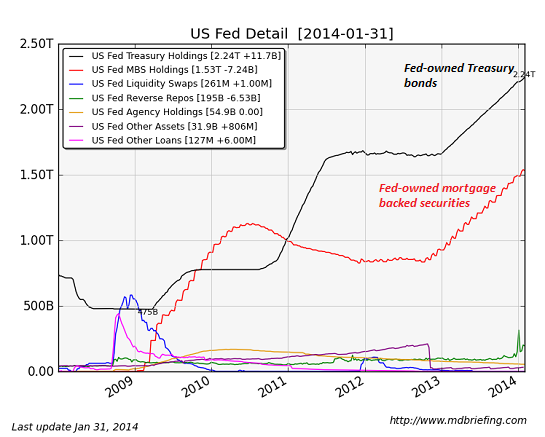

The heart of quantitative easing and ZIRP (zero interest rate policy) is the Fed's direct purchase and ownership of assets: residential mortgage-backed securities and Treasury bonds. The Fed has been operating not as the buyer of last resort but as the bidder who buys interest-sensitive securities to keep interest rates near-zero (known as financial repression). The Fed's purchases of impaired mortgages has also made its balance sheet "the place where mortgages go to die:" the Fed can hold impaired mortgages until maturity, effectively masking their illiquidity and impaired market value. We can see these two major purchase programs in this chart from Market Daily Briefing:

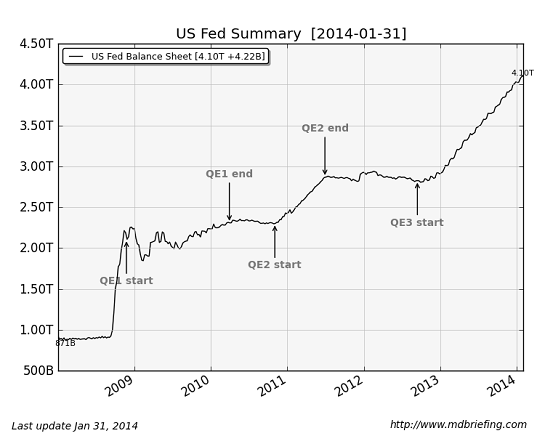

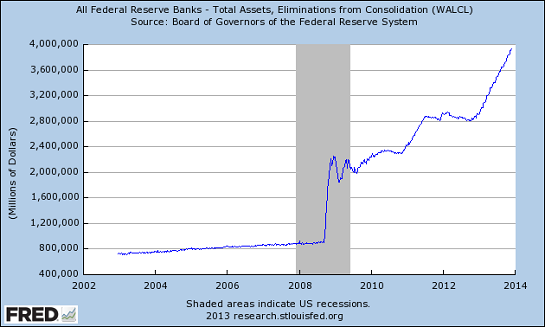

Despite all the talk of "tapering," the Fed's asset purchases on a grand scale continues:

Such a handy word, "taper:"

The Nuclear Option rests on another questionable assumption: markets only go bidless in brief panics, not because the assets have lost all value. The basic model of Fed emergency loan programs and asset-buying is 1907--a financial panic that erupts out of a liquidity crisis. In a liquidity crisis, the underlying assets supporting loans retain their market value; the problem is a shortage of credit needed to roll over short-term loans on those still-valuable assets. But what the world is finally starting to experience is not a liquidity crisis: it is a valuation crisis in which assets and collateral are finally recognized as phantom. I explained the difference between liquidity and valuation crises in In a Typhoon, Even Pigs Can Fly (for a while) (January 30, 2014). Let me illustrate why the Fed's Nuclear Option is a one-way street to oblivion. What is the market value of a defaulted student loan that has no hope of ever being repaid by an unemployed ex-student debtor? The answer is zero: the "asset" has a value of zero and will always have a value of zero. It is not "coming back." What is the market value of a commercial mortgage on a dead mall that has no hope of ever being repaid by an insolvent mall owner? The answer is zero: the "asset" has a value of zero and will always have a value of zero. It is not "coming back." The New York Times recently published an article that nails the core issue in the entire U.S. economy: the top 10% is the only segment able to support additional consumption: The Middle Class Is Steadily Eroding. Just Ask the Business World (Yahoo news version) "The Biggest Redistribution Of Wealth From The Middle Class And Poor To The Rich Ever" Explained This raises an obvious question: can the excess consumption of the top 10% support every mall, strip mall, premium outlet and retail center in the U.S.? Equally obvious answer: no. Most dead malls cannot be repurposed; the buildings are cheap shells, and while the land might retain some value for future residential housing, the coming implosion of the latest housing bubble nixes that hope: WARPED, DISTORTED, MANIPULATED, FLIPPED HOUSING MARKET (The Burning Platform). What is the value of a company's shares if that company has lost any means of earning a profit? Answer: the book value of the company's assets minus debt. Given the staggering debt load of the corporate sector, the real value of many companies once their ability to reap a real (as opposed to accounting trickery) net profit vanishes is near-zero. How about the value of Greek sovereign debt? Zero. The value of mortgages on empty decaying flats in Spain? Zero. And so on, all around the world. This leads to a sobering conclusion: Should the Fed attempt to create and maintain a bid in bidless markets, it will end up owning trillions of dollars in worthless assets--and the market for those assets will still be bidless when the Fed stops being the bidder of last resort. Let's assume the Fed's leadership will feel a desperate need to stop the next global financial meltdown in valuations. Offering trillions of dollars in liquidity will not stop sellers from selling nor magically create value in worthless assets. The Fed can only stop the selling by becoming the entire market for those assets. The list of phantom assets the Fed will have to buy outright with freshly conjured cash is long. Let's start with hundreds of billions of dollars in defaulting/impaired student loans. Once the debtors realize the system is swamped with defaults and can no longer hound them, the flood of defaults will swell. The Fed can buy as many defaulted student loans as it wants, but it will never raise the value of those loans above zero. The market for worthless student loans will remain bidless the second the Fed stops buying. The same is true of all the defaulted, worthless commercial real estate (CRE) mortgages on dead malls, decaying strip malls and abandoned retail centers: no amount of Fed buying will create a market for these worthless assets. Dead Mall Syndrome: The Self-Reinforcing Death Spiral of Retail (January 22, 2014) The First Domino to Fall: Retail-CRE (Commercial Real Estate) (January 21, 2014) There is no technical reason the Fed cannot create $10 trillion and buy up $10 trillion of worthless or severely impaired assets; the Fed can become the owner of every dead mall and every defaulted auto loan in America should it wish to. That would of course render the Fed massively insolvent, as its assets would be worth a fraction of its liabilities. But so what? The Fed can simply assign a phantom value to all its worthless assets and let them rot until maturity, at which point they vanish down the wormhole. The point isn't that "the Fed can't do that;" the point is that the Fed cannot create a bid in bidless markets that lasts beyond its own buying. The Fed can buy half the U.S. stock market, all the student loans, all the subprime auto loans, all the defaulted CRE and residential mortgages, and every other worthless asset in America. But that won't create a real bid for any of those assets, once they are revealed as worthless. The nuclear option won't fix anything, because it is fundamentally the wrong tool for the wrong job. Holders of disintegrating assets will be delighted to sell the assets to the Fed, of course, but that won't fix what's fundamentally broken in the American and global economies; it will simply allow the transfer of impaired assets from the financial sector and speculators to the Fed.

Anyone who thinks that is the "solution" should read

QE For the People: What Else Could We Buy With $29 Trillion? (September 24, 2012).

The Nearly Free University and The Emerging Economy: The Revolution in Higher Education Reconnecting higher education, livelihoods and the economy With the soaring cost of higher education, has the value a college degree been turned upside down? College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

The Nearly Free University and the Emerging Economy clearly describes the underlying dynamics at work - and, more importantly, lays out a new low-cost model for higher education: how digital technology is enabling a revolution in higher education that dramatically lowers costs while expanding the opportunities for students of all ages. The Nearly Free University and the Emerging Economy provides clarity and optimism in a period of the greatest change our educational systems and society have seen, and offers everyone the tools needed to prosper in the Emerging Economy. Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA). We are not powerless. Once we accept responsibility, we become powerful. Read the Introduction/Table of Contents

Kindle: $9.95

print: $24

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

"You shine a bright and piercing light out into an ever-darkening world."

Subscribers ($5/mo) and those who have contributed $50 or more annually

(or made multiple contributions totalling $50 or more) receive

weekly exclusive Musings Reports via email ($50/year is about 96 cents a week).

Each weekly Musings Report offers five features:

At readers' request, there is also a $10/month option.

What subscribers are saying about the Musings

(Musings samples here):

The "unsubscribe" link is for when you find the usual drivel here

insufferable.

I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Making your Amazon purchases through this Search Box helps support oftwominds.com at no cost to you:

Add oftwominds.com

|