|

|

|

|||||||||

|

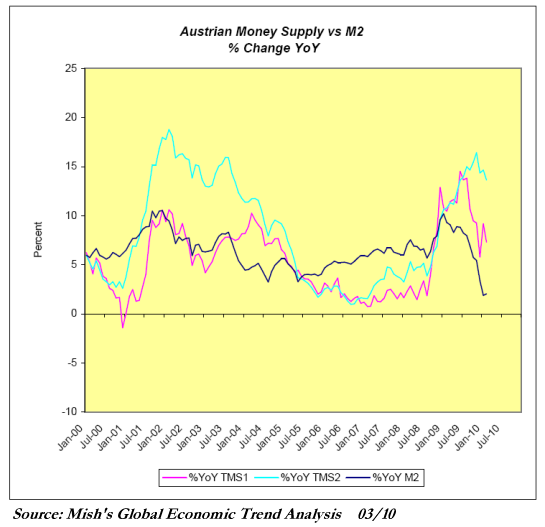

The Contrarian Trade of the Decade: the U.S. Dollar (March 22, 2010) Just as a speculative thought experiment: perhaps the great contrarian trade of this decade is cash/the U.S. dollar. The majority of economic observers seem convinced that the dollar is doomed, and not in some distant future. The basic reason for this unanimity is the reasonableness of the basic thinking, which goes like this: The Federal Reserve and the U.S. Treasury are "printing money" and flooding the economy with easy money and credit, and the result of this debasement of the nation's currency will be rampant inflation. In other words, if a nation greatly expands its money supply without expanding its production of goods and services, then all that surplus money ends up chasing scarce goods and services, and you get inflation: the same sum of currency buys less and less goods and services. This is the goal of State policy, according to the standard line of thinking: The only way the Federal Reserve and the Treasury can "save" the debt-burdened U.S. economy is by creating high inflation, which enables debtors to repay debt with "cheaper" dollars. Everyone who owns debt or low-yield bonds will lose huge chunks of their assets, but for no-asset debtors, inflation will be the cat's meow. But perhaps this thinking is wrong on virtually every important count. I am indebted to my tireless and insightful blogging colleague Mish for an understanding of money supply: True Money Supply. Here is Mish's chart of three ways to calculate money supply, and he argues persuasively for TMS1 as being the most accurate:

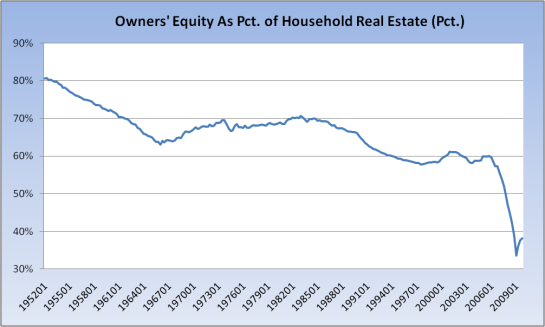

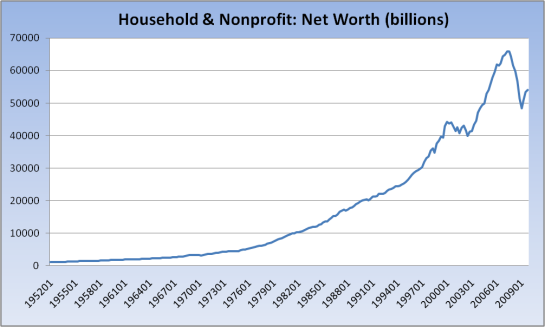

While the Federal Reserve successfully goosed money supply in their massive "quantitative easing" campaign, money supply is no longer expanding at a fast clip. The critical distinction between printing press and credit is rarely discussed: is money literally being printed or is it credit-based? The distinction has profound consequences. If a government prints stacks of currency and then distributes the freshly conjured money via helicopter drops (in the visually compelling imagery of Fed Chairman Ben Bernanke's famous "helicopter drop" quip), then the money supply has been expanded and distributed into the economy where it then leads to inflation if the production of goods and services lags money growth. But if a government--for instance, the U.S. Treasury--prints bonds and sells those bonds to raise cash to distribute in the economy, that is not "printing money." The Treasury bonds are traded for cash presented by purchasers; the money already exists and is simply being transferred to the State for distribution into the economy. If money is being created via the magic of fractional reserves (that is, via bank credit), then it does not flow into the economy if those banks do not lend it and if consumers do not borrow it. As Mish has repeatedly observed, banks cannot be forced into lending nor consumers into borrowing. It seems the money "created" by the Federal Reserve and lent to private banks at near-zero interest rates is simply sitting in the banks as reserves to offset their continuing horrendous losses. As a result, it is not flowing into the economy, and thus it cannot trigger inflation. In contrast, a State such as Zimbabwe does run its printing presses to create money, and this explains why it suffers from hyper-inflation. It can be argued that the billions of dollars the Fed orders into existence and then trades for Treasury bonds (i.e. to buy T-Bills) is in fact "freshly created money" that flows into the economy via Federal deficit spending. True, but then the question becomes, do these purchases of Treasuries add enough to the $13 trillion U.S. economy to offset the reduction in credit as people and businesses either pay down debt or write off uncollectable/bad debt? According to the Wall Street Journal (Drought of Credit Hampers Recovery), consumer credit outstanding has shrunk some $119 billion, or 4.6%, from its peak in July 2008, to $2.46 trillion. Add in the mortgages paid down, paid off or written down in excess of new mortgages issued, corporate debt retired or written off, etc. etc., and it seems the deleveraging that is underway in both consumer and corporate balance sheets is reducing credit and money supply by hundreds of billions of dollars. The Fed purchasing $300 billion or even $500 billion in Treasury bonds simply doesn't pump enough money into a deleveraging $13 trillion GDP-economy to create inflation. It merely offsets some of the destruction of credit going on at every level of the economy. Thus you can have a central bank shoveling credit-created money into private banks where it sits, never entering the economy at all. How can that create inflation? Indeed, as has often been noted by Mish and others, this is what has happened in Japan for the past two decades: the central bank shovels money into private banks, who either engage in "carry trade" activities (borrowing at near-zero interest and then moving the money overseas to earn a decent yield elsewhere for easy profits) or they stash the funds to offset their ongoing losses in defaulted/impaired portfolios. Those portfolios of impaired assets in Japanese, U.S. and European banks--just how much are they worth in a transparent "marked to market" setting? How many trillions of dollars in mortgage-backed securities, household debt, corporate debt and defaulted/impaired sovereign debt do these banks hold? If they had to sell those assets in an open market, how much would they fetch? How big would the losses be? Nobody knows, but we can guess the losses are easily in the tens of trillions of dollars. The accounts of banks keeping defaulted mortgages on the books are legion; Japan has played the "waiting for better asset prices" game for decades, and now U.S. banks are playing the same game: accepting interest-only payments of a few hundred dollars from homeowners as an accounting gimmick to keep the loan on their books as "performing." This artifice does nothing to clear the actual bad debt. And how about all those impaired off-balance sheet liabilities? Regulators are not only allowing financial institutions to continue marking assets to fantasy, they are also allowing them to continue holding assets off their legitimate balance sheets. The ever-astute Karl Denninger of the Market Ticker blog has relentlessly exposed these frauds and accounting tricks. Since we live in a credit-based monetary system and economy, then income and collateral are the foundations of credit/borrowing. Unfortunately for those wishing for vast expansions of borrowing to fuel inflation, real estate collateral is not just impaired, it has fallen to historic lows. We can only wonder what this chart would look like if all real estate was truly marked to market:

The point is that the collateral represented by the average U.S. household's primary store of wealth--their home--is near-negligible. Why? As noted above, houses are still being valued far above their true market value, so any reduction in value comes straight off the equity. For example, a house valued at $300,000 on the bank's books justifies the $270,000 mortgage being held at full value. The homeowner supposedly has $30,000 in equity/ collateral. But if the house is actually marked to market at $250,000, the owner's collateral vanishes and the bank's "asset" (the mortgage) also declines in value.

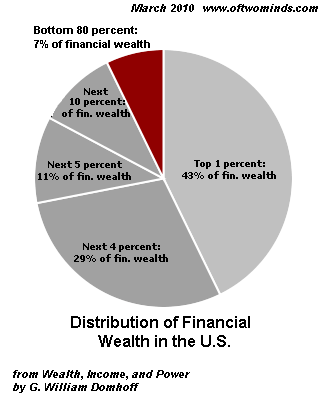

Put all this together and we can deduce that those homeowners who might desire to extract some equity from their homes via borrowing have no collateral left to borrow against. What about other collateral, such as income? As we all know, functional unemployment/underemployment is around 17%. According to the BEA, personal income has declined by over $200 billion from 2008 to 2009. (Subtract government transfers and the number is more like $600 billion.) The BEA table reveals that "Net increase in household liabilities" hit $1.8 trillion in 2006 and $1.4 trillion in 2007, and then fell to $146 billion in 2008. Households are no longer borrowing (adding liabilities). Meanwhile, savings jumped from $178 billion in 2007 to $470 billion in 2009. Mortgage debt rose by $1.1 trillion in 2005, $1 trillion in 2006, $686 billion in 2007--and then fell by $106 billion in 2008. No data is available yet for 2009, but you can bet both mortgage debt and new liabilities continued plummeting. So household incomes have fallen, meaning there is less collateral for new borrowing, and new liabilities and mortgages have both collapsed from nearly $3 trillion in 2006 to $46 billion in 2008. Yes, from $3 trillion in new borrowing in 2006 to a total of $46 billion in 2008. That is deleveraging, and adding $300 billion in money supply via Federal Reserve buying of T-Bills is offsetting a meager 10% of that decline in household credit. Now that we've seen that housing and income collateral have fallen off a cliff and are not recovering, and that households are deleveraging ($3 trillion they were borrowing in 2006 has fallen to a mere $46 billion--more or less statistical error or pocket change in a $13 trillion economy)--then we might ask if those who still have assets would wish to leverage them into more borrowing/debt. The vast majority (83%) of other financial assets are held by the top 10% households. here is a chart I reprinted recently in The Stock Market As Propaganda (March 10, 2010).

Equities (stocks) currently represent about $11.4 trillion of the total $33.3 trillion in financial assets. Business assets and real estate make up the remaining $20 trillion in total assets. According to the BEA, total household assets fell from $63.9 trillion in 2007 to $52.9 trillion in 2008--a decline of $11 trillion. The recent stock market rally and "recovery" in housing has caused a blip up in total assets, which now appears to be rolling over.

Since the bottom 80% of U.S. households only hold 7% of financial assets ($2.3 trillion spread amongst 105 million households), then their ability to leverage their declining income and modest assets into huge dollops of new debt is somewhere between low and zero. Recall that households added $3 trillion in new borrowing in 2006 alone. So those heady bubble days of credit/money supply growth are gone for good. Since the top 10% households own $27 trillion in financial assets, we might ask what need they would have for new debt. We might also ask what might happen if nobody comes forward to buy $1.5 trillion in new Treasury debt every year (money needed to fund the Federal deficit of $1.5 trillion a year) at very low yields. I outlined the high probability of this happening in The Trouble With Bonds (March 18, 2010). Interest rates will rise. Recall that the Fed does not set yields for Treasury bonds; that is set by the bond market (supply and demand). The only way for the Fed to influence the yield of T-Bills is to buy them outright, as it has been doing heavily of late. Since every other major nation is also selling bonds to fund deficits, then we can anticipate some lively competition for investor's cash. In the standard view that "governments just print money," then why governments sell bonds is never explained. Why don't all governments just print up money and spend that? Why go to all the trouble of selling bonds to raise cash to fund deficits? It comes down to the distinction between credit-based systems and currency-based systems. Inflation is impossible in credit-based systems when credit is being paid down/destroyed/ written off and banks are wary of lending/risk and consumers refuse to (or cannot) borrow. We might also ask what might happen to stocks, bonds and real estate valuations if interest rates rise: they tank as I explained in What If (Almost) All Assets Fall Together? (March 11, 2010). As a side-effect, the meager assets of the bottom 90% of U.S. households would fall, and the "smart money" might well decide selling out before further declines occur is the wisest capital-preservation strategy. Since so much debt is dollar-denominated, then there will be demand for dollars to pay down debt. That is the essence of deleveraging. And since other assets will be falling as interest rates rise and risk aversion returns with a terrible vengeance, then "cash will be King." Dollars will rise in value, and the best and safest return on capital will be money-market funds or short-term notes. Rather than doom the dollar, these trends suggest the dollar could rise in purchasing power and demand for years to come. I know this is contrarian, but ponder the distinction between "printing money" and selling bonds/attempting to expand credit in a credit-averse, collateral-impaired system. This might be one of the most important bits I write this decade. Or then again, maybe not. Only time will tell. Before chastizing me for rampant hyperbole--"most important story of the decade, bah"--please consider The Most Important Chart of the Century. Now the chart is extremely important, and I recommend reading this story, but the century is a bit young to declare "the chart of the century." One wonders what the "chart of the century" would have been in 1910, and how prescient we would find it in hindsight. Let's say this is one of the most important charts of the past 50 years, which is entirely supportable.

The charts simply shows that adding debt no longer adds to GDP. So even if the Fed

were able to force banks to lend to poor credit risks and deleveraging borrowers

lost their sanity and added to their liabilities, then the economy still wouldn't

grow/"recover." The "reflating the credit bubble" game is over.

DailyJava.net

is now open for aggregating our collective intelligence.

Of Two Minds is now available via Kindle:

Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2010 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||