|

|

| weblog/wEssays archives | home | |

|

How Many Foreclosures Will Hit the Market? (May 1, 2006)  OK people, stay sharp. We're going to thread our way through a lot of housing

statistics and reach a mind-boggling conclusion: 5 million foreclosures,

5 million investment/2nd homes dumped on the market and bank/thrift losses of $500 billion.

Farfetched? Read on.

OK people, stay sharp. We're going to thread our way through a lot of housing

statistics and reach a mind-boggling conclusion: 5 million foreclosures,

5 million investment/2nd homes dumped on the market and bank/thrift losses of $500 billion.

Farfetched? Read on.

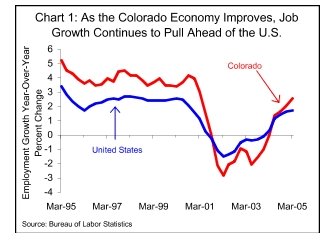

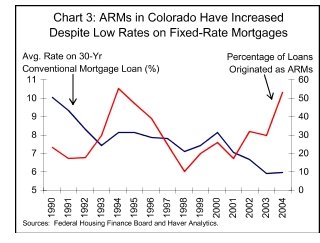

First up is housing Bull Michael Youngblood, managing director of asset-backed securities (a.k.a. mortgage-backed securities) at Friedman, Billings Ramsey who states in this week's Barron's: "What dominates the mortgage market is income." In other words, if people have jobs, housing will continue to rise. He goes on to assert that interest-only loans are not more dangerous than fixed-rate mortgages. Leaving aside that Mr. Youngblood earns his living selling "securitized" mortgages (if people stop paying the mortgage, the value of the security plummets--not that you'd hear that from Mr. Youngblood), let's look at his thesis.  The chart above shows job growth in Colorado to be better than in the nation as a whole

(unemployment is a low 4.7% nationally). Next, look at the chart of

Colorado adjustable-rate mortgages (ARMs). Even as fixed-rate mortgage rates dropped to historic lows,

over 50% of the loans in Colorado were ARMs.

The chart above shows job growth in Colorado to be better than in the nation as a whole

(unemployment is a low 4.7% nationally). Next, look at the chart of

Colorado adjustable-rate mortgages (ARMs). Even as fixed-rate mortgage rates dropped to historic lows,

over 50% of the loans in Colorado were ARMs.

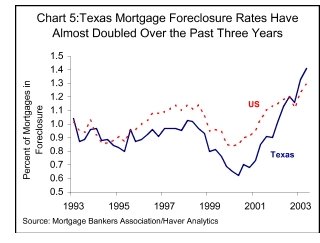

According to Mr. Youngblood, everything should be hunky-dory. But the reality is that foreclosures are skyrocketing in Colorado, and are 3 times higher than the national average; from National Foreclosures Up 63 Percent From a Year Ago: Colorado’s foreclosure rate leapfrogged to highest among the states thanks to a 31 percent increase in new foreclosures from the previous month. The state reported 5,392 properties entering some stage of foreclosure in March, a foreclosure rate of one new foreclosure for every 339 households — more than three times the national average.  So much for Youngblood's cheery (if baseless) thesis. Here is a state with strong job growth and plentiful

ARMs--and foreclosures are leaping. The stark reality of foreclosures is not isolated

to Colorado, as this chart of Texas foreclosures shows. The situation in Boston is equally

perilous, as reported in the

Homeowners stretched perilously from the

Christian Science Monitor of 3/21/06:

So much for Youngblood's cheery (if baseless) thesis. Here is a state with strong job growth and plentiful

ARMs--and foreclosures are leaping. The stark reality of foreclosures is not isolated

to Colorado, as this chart of Texas foreclosures shows. The situation in Boston is equally

perilous, as reported in the

Homeowners stretched perilously from the

Christian Science Monitor of 3/21/06:

Fully 27.1 percent of Boston's homeowners with a mortgage spent at least half their gross income on housing in 2004, according to the latest census figures available. Those costs, which include utilities and insurance as well as mortgage payments, were more than double the national rate of 11.7 percent and topped New York (25.9 percent), Los Angeles (26.5), San Francisco (20.4), and Chicago (20.3). Of the 25 biggest cities, only Miami had a higher rate (35.8 percent).USA Today chips in with this story on the woes facing the millions of homeowners stuck with ARMs: Some homeowners struggle to keep up with adjustable rates When they refinanced their home two years ago to pay off some bills, Robert, now 78, was working as a deliveryman. But his employer went out of business last April. Now he and Lorraine, 72, a retired nurse, are both seeking work. The rate on their mortgage has jumped from 7% to 10.5%.Hmm, nothing like a little media snooping to pry a fixed-rate mortgage out of the woodwork, eh? This tale reveals how subprime lenders have taken advantage of desperate/ hopeful/ignorant homeowners who are stunned to find their rates rising 3.5% in one bound. Realtors, of course, couldn't be happier selling empty condos and houses by the millions to unwary investors. Second Home Sales Hit Another Record in 2005; Market Share Rises 27.7 percent of all homes purchased in 2005 were for investment and another 12.2 percent were vacation homes. All together, there were 3.34 million second-home sales in 2005, up 16.0 percent from an upwardly revised total of 2.88 million in 2004. The market share of second homes rose from 36.0 percent of transactions in 2004 to 39.9 percent in 2005.As the market softens, investors are finding that they can't dump their units for love nor money. Here is a Washington Post story investors hurting; Doors Close for Real Estate Speculators After Pushing Up Prices, Investors Are Left Holding Too Many Homes. Just for context: according to the National Association of Realtors, There were 7,072,000 existing-home sales in all of 2005, up 4.2 percent from 6,784,000 in 2004. This is the fifth consecutive annual record; NAR began tracking the sales series in 1968. According the U.S. Census Bureau, 1.3 million new homes sold in 2005.The Census Bureau also reports that there are approximately 75 million homeowners in the U.S., and 33 milllion occupied rental units.  Let's summarize:

Let's summarize:

In a nutshell: in the past 3 years, 10 million people signed ARM mortgages which will reset soon, and 10 million housing units were sold to investors. Foreclosures are already rising, even though job growth is strong and unemployment is low. In addition, 4 million recent homebuyers are subprime risks whose grasp on their homes is tenuous indeed. If 5 million marginal bubble-buyers fold their hands due to ARM resets or job loss, what will that do to the value of those 10 million investment units? Let's say the resulting drop in values causes half of those empty, cash-flow negative units to get dumped on the market (or foreclosed upon). Who's going to buy these 10 million properties?  One last chart. Bank reserves--the cash lenders keep to cover "bad loans"--is at an all-time

low. That leaves lenders extraordinarily vulnerable to losses should foreclosures rise.

The expert quoted above estimated bank and thrift losses of $100 billion should 1 million

homes go into foreclosure, so what happens if 5 million properties default? Simple

extrapolation suggests losses would exceed $500 billion. Does that sound extreme? Not

at all, when you consider that the dot-com bubble bursting erased at least $1 trillion in

equity. Compared to that, a mere half-trillion in losses doesn't seem unrealistic.

One last chart. Bank reserves--the cash lenders keep to cover "bad loans"--is at an all-time

low. That leaves lenders extraordinarily vulnerable to losses should foreclosures rise.

The expert quoted above estimated bank and thrift losses of $100 billion should 1 million

homes go into foreclosure, so what happens if 5 million properties default? Simple

extrapolation suggests losses would exceed $500 billion. Does that sound extreme? Not

at all, when you consider that the dot-com bubble bursting erased at least $1 trillion in

equity. Compared to that, a mere half-trillion in losses doesn't seem unrealistic.

For more on this subject and a wide array of other topics, please visit my weblog. copyright © 2006 Charles Hugh Smith. All rights reserved in all media. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

||

| weblog/wEssays | home |