|

|

|

Inventory and Foreclosures: Is The Bottom Really In? (May 2, 2008)  The cheery prospect of a "bottom" in housing prices is already being

anticipated. Will the bottom be next quarter, or (gasp) all the way out

in 2010?

The cheery prospect of a "bottom" in housing prices is already being

anticipated. Will the bottom be next quarter, or (gasp) all the way out

in 2010?

Perhaps one way to tell is to look at the inventory of unsold/vacant houses. (Recall that a vacant house in a declining market is not an rising asset--it's a capital trap.) Let's start with a snapshot of current trends (Bloomberg): U.S. Home Vacancies Rise to Record on Foreclosures

A record 18.6 million U.S. homes stood empty in the first quarter as lenders took possession of a growing number of properties in foreclosure.

Now let's review some basic data I assembled in Will Delinquencies Trigger a New American Revolution? (April 7, 2008)

population of the USA: 303 million (as per US Census website)Put all this together and what can we conclude? 1. Perhaps 7 million of the vacant 19 million empty dwellings are true second homes. 2. The other 12 million are vacant but the owners would like to either sell or rent them out. So how many other homes are in the foreclosure/inventory/vacant pipeline? From my previous entry (link above):

The delinquency rate for all mortgages climbed to 5.82 percent in the fourth quarter. That was up from the 5.59 percent in the third quarter and was the highest since 1985. Payments are considered delinquent if they are 30 or more days past due.U.S. Foreclosure Filings Double in First Quarter

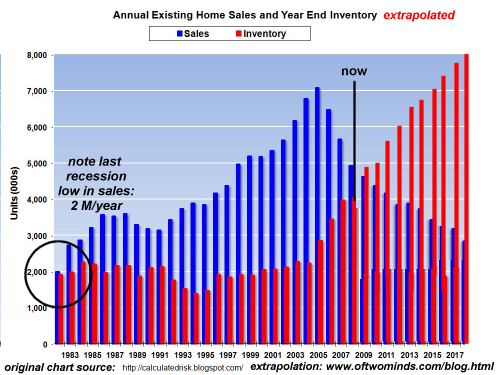

Almost 650,000 properties were in some stage of foreclosure during the quarter, or 1 in every 194 U.S. households, Irvine, California-based RealtyTrac Inc., a seller of foreclosure data, said today in a statement. The number was 112 percent above a year ago. Nevada, California and Arizona had the highest rates.Now let's ask: how many more homeowners are at risk of being foreclosed/walking away? I've looked at this question twice in the past two years, and since the data is still valid, so are the conclusions: Can 4% of Homeowners Sink the Entire Market? (February 21, 2007) How Many Foreclosures Will Hit the Market? (May 1, 2006) I know an additonal 5 million homes dumped into inventory of unsold/abandoned/vacant dwellings seems like a lot, but that's only 10% of existing mortgages (50 million) and only 5% of U.S. households (105 million). Let's consider a chart I've prepared of inventory and sales, and cover the trends which are firmly in place which make this scenario so likely:

The "happy story" that a bottom is in sight being bandied about is based on fantasies unsupported by powerful trends with a lot more room to run. The happy story requires a belief that sales will stay high enough to absorb inventories that are stabilizing. Nice, but what if the trends are precisely the opposite? In fact, sales are plummeting and inventories are rising. Let's consider other trends that are rarely noted but extremely powerful. 1. Most buyers are selling their existing house. New buyers entered the market in the bubble for two reasons: cheap no-down, no-doc lending, and the desire to speculate. (Recall that 40% of all the homes/condos purchased in the bubble years were bought by speculators, some of whom offered the fig-leaf of a "second home" to secure better mortgage terms.) If buyers are adding another home to inventory, then how does inventory drop? As I detailed in Can 4% of Homeowners Sink the Entire Market?, virtually everyone who is above the poverty line in the U.S. already bought a house. The notion that population growth will magically produce millions of new home buyers is unlikely for two reasons: 2. Stricter lending guidelines and the need for 20% down removes most people from the buying pool. With homeownership at record highs (68% or so), the idea that millions of young people and immigrants will a) find good-paying work in a recession b) have 20% down and c) have a good credit history is assuming a tremendous amount. There is very little data or even anecdotal evidence to support this thesis. 3. Density can rise in recession. As I demonstrated in Brain-Dead Predictions about Housing (January 2, 2008), 5% upswings in population can and do occur without any increase in the number of dwellings. It's called moving back home, doubling up, renting out a room. This means 5 million U.S. households could quite easily no longer require a separate dwelling. That would push another 5 million units onto the vacant/for-sale/rental markets. Take 5 million foreclosures (5 million recession-downsized households) and you can easily add another 5 million vacant units to the current 12 million. Meanwhile, over on the sales side of the ledger, let's look at what happened to sales in the last "real" recession of the early 1980s: 4. Sales dropped to 2 million units a year. And what data suggests this isn't the end-point of the current downtrend? Put together an inventory of vacant dwellings that could easily top 20 million and a sales per year figure which could easily drop in half and what do you get? A gigantic supply-demand imbalance which will have large effects on price. I am also surprised few if any commentators note these other factors: 5. There is nothing sacrosanct about a "second home." It can easily become a primary dwelling. As Baby Boomers retire, many will sell their primary residence and move to the second home they already own. And what does that trend do to inventory? It increases it. 6. As Baby Boomers retire, they will liquidate assets to pay for the niceties of life, like "gap" health insurance and a new knee/hip. And what will they sell? How about Mom and Dad's old house, which is currently a capital trap, sitting empty now that they're gone. And how about that rental house we bought in the bubble? Being a landlord is such a hassle. Dump it. The vacation condo? Dump that too before it loses any more value. The millions of investment properties purchased in the bubble will be offloaded for any number of reasons. Owners will tire of the losses, or tire of being absentee landlords or they'll need to money for retirement or medical costs. Or they'll go bankrupt and the property will be liquidated/handed over to creditors. And last but not least: 7. Home builders and developers will continue to build more homes, even in a recession. It's build or die, and with the permits pulled and the property sitting there requiring interest payments, there are still incentives to build and dump new homes and condos in "still strong" markets. Let's say new homes drop from almost 2 million a year down to 500,000 a year in the recession. That's still another half-million homes added to inventory. In conclusion: there is plentiful evidence that sales will continue heading down, perhaps to their previous recession low of 2 million (existing homes) sold per year, and that the inventory of vacant dwellings waiting to be sold or rented will keep rising for a long time to come. I haven't even mentioned the nightmare scenario, which is money for mortgages becomes scarce. Interest rates may still be low, but if investors no longer care to risk buying mortgages--why gamble your money on the slim chance housing will stop declining in value?--then loans will be increasingly unavailable, regardless of the low Fed Funds Rate. Without cheap, easy credit, very few can afford to buy a house at any price.

All evidence suggests the demand-supply imbalance in housing will only worsen for

many years to come. As the saying goes in the stock market: beware trying to catch a

falling knife (e.g. falling prices).

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Jerry & Rosanne A. ($21), for your very generous multiple contributions to this

site.

I am greatly honored by your support and readership.

For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||