|

|

|

When Will Housing Really Bottom? (Part I) (October 6, 2008) This week's theme: How Long Will the Coming Depression Last? The financial punditry confidently state that the "recession" won't end until housing "recovers." So our first question is: When will housing really bottom? The standard Punditry Party Line (PPL) in the MSM (mainstream media) is that housing will bottom in 2009 and then start "recovering" in 2010. This is (surprise!) wildly optimistic. A fact-based analysis suggests 2012 or 2013 as the most optimistic near-term trough, followed by years of stagnation. Oh, and that's the best-case scenario. Worst case scenario is the complete repudiation of three generations of American cultural/financial faith that "housing will always be your best wealth-building investment." In other words, people finally realise that buying real estate is a capital trap and a poor use of their money. That may or may not happen, but it is certainly in the realm of possibility. Let's start by setting up some essential context for the housing market. 1. Housing depends on mortgages, i.e. borrowing vast sums of money. That money begins as savings, i.e. capital, which is then leveraged in our wonderful banking sector about 12 to 1, meaning if savers deposit $100 in a bank, the bank can write a mortgage for $1,200. Yes, there used to be these amazing things called mortgage-backed securities (MBS), which enabled banks to bundle all their mortgages and then sell them to investors/speculators. This got the mortgages off the bank's balance sheet, clearing the way for the bank to write another $1,200 in mortgages for each $100 in deposits. 2. But the market for mortgage-backed securities has just about vanished, so now banks and lenders will actually have to keep mortgages on their own books. From Doug Nolan's Credit Bubble Bulletin: (courtesy of U. Doran):

There was no Asset-Backed Securities (ABS) issuance this week. Year-to-date total US ABS issuance of $129bn (tallied by JPMorgan's Christopher Flanagan) is running at 26% of comparable 2007. Home Equity ABS issuance of $303 million compares with 2007s $224bn. Year-to-date CDO issuance of $24bn compares to the year ago $286bn.This is an astounding collapse of the very markets which birthed the housing bubble. Strike One against housing "recovery": collapse of the MBS, home equity (HELOC) and CDO markets. The point is simple: lending/writing new mortgages ultimately depends on savings, i.e. capital. Here's a snapshot of U.S. savings:

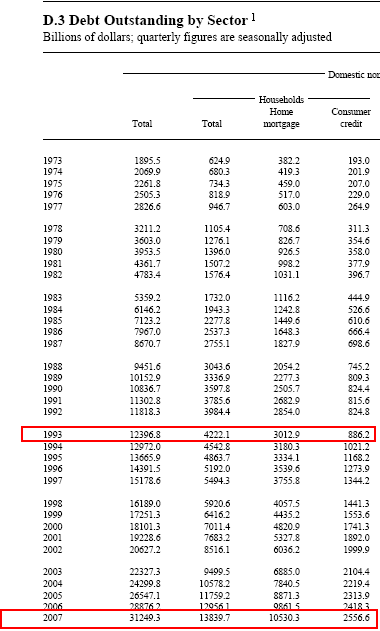

Gee, it doesn't look like we're accumulating much capital, does it? Many pundits like to ignore this abysmally low capital formation by clucking about all those trillions in 401K accounts and IRAs. But much of that is restricted to stock and bond mutual funds which do not overlap much with the mortgage market. Strike Two against housing "recovery": inadequate capital/savings. 3. The nation is drowning in debt on all levels. The notion that we will collectively be ready, willing and able to add a couple trillion dollars in new mortgages by next year is simply unrealistic. Look at how total consumer debt has tripled since 1993:

Meanwhile, GDP only doubled between 1993 and 2007 ($6.6 trillion to $12.8 trillion). Strike Three against housing "recovery": debt has far outpaced actual economic growth. (First batter Bernanke, you're out.) 4. The banking sector is in trouble, and this chart reveals part of the underlying reason: a credit bubble of staggering proportions.

Strike Four against housing "recovery": the credit bubble has burst and the entire U.S. banking sector is melting down. For a snapshot of financial cardiac arrest, here is Nouriel Roubini's report, courtesy of frequent contributor U. Doran: Financial and Corporate System is in Cardiac Arrest: The Risk of the Mother of All Bank Runs. 5. The "lender of last resort"--the Federal government--is running gargantuan deficits even before the bailout and Federal Reserve loan largesse ($600 billion and counting) is factored in. Frequent contributor Michael Goodfellow located a fascinating and deeply disturbing data series on the U.S. Treasury site for "Debt to the Penny". According to these up-to-date figures, the Federal deficit has increased $1.061 trillion in only a year. Michael wrote:

Request 10/1/2007 to 10/1/2008 and you get a daily table. Here are the first and last lines:(Note: this last entry reflects the fact that the government "borrows" the Social Security surplus every year to spend and enters the theft as a "debt we owe ourselves.") The MSM has reported that the Federal deficit is on track to hit $500 billion this year, yet here we see that it has already increased $800 billion, even without accounting for the $600 billion the Fed has loaned banks or the bailout costs of $850 billion ($700 billion to "friends of Hank" and $150 billion in pork/tax credit giveaways). From the Christian Science Monitor in April 2008:

This February, in the president's annual budget submission to Congress, the White House Office of Management and Budget (OMB) predicted the federal deficit for fiscal year 2008 would come in at $410 billion.From the Washington Post 9/10/08: Federal Shortfall To Double This Year:

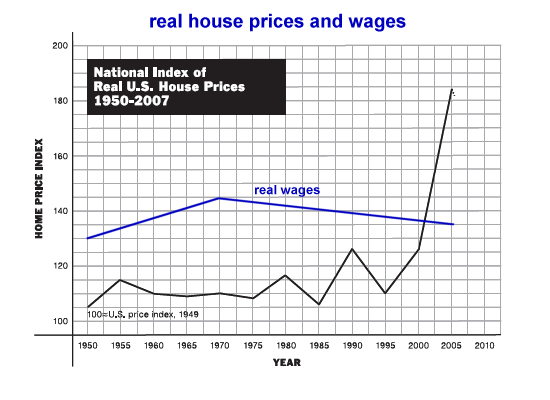

A weak economy and a sharp increase in government spending will drive the federal budget deficit to a near-record $407 billion when the budget year ends later this month, and the next president is likely to face a shortfall in January of well over $500 billion, congressional budget analysts said yesterday.Note to MSM: the budget deficit has already hit $800 billion, apparently when you weren't looking. Strike five: the Federal government's ability to "bail out" housing is now severely restricted by trillions of dollars of "unexpected" deficit spending/borrowing. Just like the banking sector is it trying desperately to revive, the Federal government budget is purposefully opaque: the full cost of the wars in Iraq and Afghanistan is held out of the regular budget to cloak the true costs; the Federal Reserve's balance sheet has declined from $800 billion in cash to less than $200 billion, and hundreds of billions more have been "injected" into the global financial system by the Treasury in a vain attempt to "increase liquidity." None of this shows up in the budget. The actual amount of money the Federal government has thrown at the credit crisis is undoubtedly already well above $1 trillion, even before the TARP bailout's $700 billion has been tapped. 6. In constant dollars, housing leaped 50% in the bubble even as wages have stagnated.

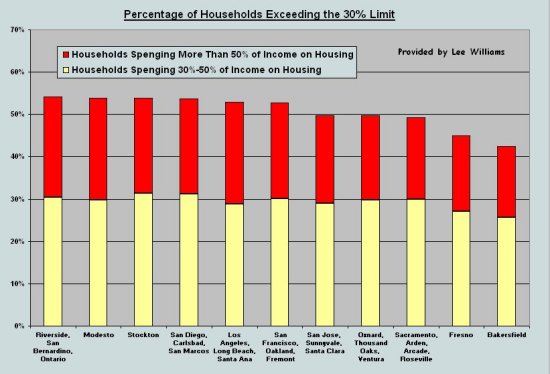

In other words, housing has historically been correlated to wages/income--which makes common sense. The bubble broke that correlation, and now what was unsustainable--housing rpices rising far above wages--must return to historical averages. Strike six: housing must return to historic correlations to wages/income. (Batter Hank Paulson: you're out.) Note what happens to wages/income in a deep recession: they drop, meaning housing will have to drop even further to restore the historic correlation. For more evidence of this, consider this chart which depicts how many California home owners are paying absurdly unsustainable percentages of their income on housing:

7. The history of recent housing bubbles around the globe suggest that the price of houses will eventually drop all the way back to pre-bubble valuations.

Strike seven: bubble-era prices must decline all the way back to their starting point, and we are far from that endpoint in most of the country. 8. The entire banking system which generates the mortgages, HELOCs and construction financing on which real estate depends is about to implode due to derivatives exposure.

The housing bubble and the credit bubble are as interwined as two strands of DNA. Thus once-obscure derivatives such as CDS (credit default swaps) are now blowing up banks around the globe, crippling the entire "empire of debt" which sustained the global housing bubble. Strike eight: the derivatives-based "shadow banking system" of global finance is imploding, and will never return to its bubble-era heyday. 9. The value of real estate (and hence all mortgage-backed security) collateral is now unknowable, and therefore banks are refusing to lend. This is common sense. If you're asked to loan money with a house as collateral, and that collateral is in free-fall/depreciating rapidly, then how can you possibly assess your risk of future loss? Adding to this insecurity is the impossibility of valuing tranches of mortgage-backed securities which bundled hundreds or thousands of individual mortgages of varying risks. Transparency was deliberately tossed under the wheels as a prerequisite to selling risky asset-backed securities as low-risk. For lending and thus housing to stabilize, transparency has to return to the markets--in full. We are far from transparency, as it is widely admitted that most of these asset-backed securities are difficult or impossible to price. Strike nine: financial gamesmanship and opacity have doomed the global financial system and thus housing to years of distrust and uncertainty. Batter G.W. Bush, you're out.) For a breathtaking description of just how fast the fragile "empire of debt" is crumbling, please read Doug Nolan's notes to his latest Credit Bubble Bulletin (link above):

Looking back, Total Non-Financial Debt (NFD) expanded $578bn during 1994. By 1998, NFD growth for the year had surpassed $1.0 TN. Non-Financial Credit increased $1.153 TN in 2001, $1.415 TN in 2002, and $1.676 TN in 2003, before reaching the $2.0 TN milestone in 2004. Incredible as it was, debt expansion then surged over the next fateful three years. Growth rose to $2.319 TN in 2005, $2.428 TN in 2006 and then to last years record $2.561 TN.The punditry, the cheerleaders and even the "responsible" MSM are all loudly proclaiming 2009 or 2010 as the "bottom" in housing and then away we go to the bubble-era races again. Please consider Nolan's report before placing any trust or faith in these happy stories. If history is any guide, working through these excess of opacity, debt and leverage will take a decade or even longer.

I would guess five years, i.e. 2013, would be a near-miraculously rapid rebuilding

of trust and capital. A more measured view would look out as far as 2020, i.e.

12 years hence, for a "real bottom" following history's greatest credit/housing bubble.

We are still a ways off on our current timeline leading to a contemporary Marie Antoinette statement about bread and cake. I suspect when that moment arrives in a marbled room on this side of the Atlantic, it will either be tightly controlled or leaked by design. However, we are now at a point where the well-powdered whisper blowing upon the tiny spark of public anger seems to be If they have two slices of bread, then take their little pat of butter. The No Banker Left Behind Bill (Chuck D., September 29, 2008) I have been mulling over the proposed bailout bill (which I have decided should be called the No Banker Left Behind Bill). I have the feeling that no matter what they do, something big this way is coming. I just dont know what form it will take. There Is Ultimately No Gaming the System: When the Micro Crash Reflects the Macro Crash (Zeus Y., September 29, 2008) The proposed 700 billion dollar bailout cannot really work from a system level. I know its real intention is to cover the butts of Wall Street investors, but you have the same problem in macro that homeowners have in micro. Nobody knows what homes are worth right now, so buyers are sitting it out. It isnt about restricted credit (even though that is a factor). It isnt about being too cash strapped to make a down payment (though that too is a factor). Its about not wanting to be suckered into buying something that may still be overpriced.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Jennifer F. ($15), for your very generous donation

to this site.

I am greatly honored by your ongoing support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||