|

|

|

|||||||||||||

|

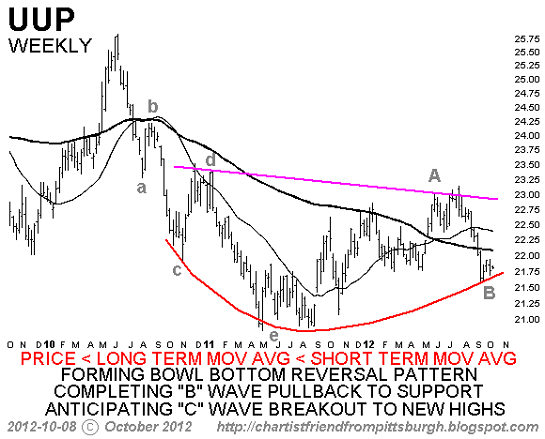

What Will Benefit from Global Recession? The U.S. Dollar (October 9, 2012) Understanding the euro's failure and Triffin's Paradox helps us understand why the dollar will rise significantly in the years ahead. Many times what "should" happen does not happen. For example, global stock markets "should" decline as the global economy free-falls into recession, as global recession is not exactly an ideal scenario for rising corporate sales and profits or demand for commodities. Yet global markets are by and large rising significantly. Sometimes what "should" happen is simply being delayed. In other cases, some other dynamic is at work. Stock market bulls, for example, say the "other dynamic" is global money-printing by central banks, and this "easing" will power stocks higher even as sales and profits sag. Analysts who believe fundamentals eventually over-ride monetary manipulation believe the stock market decline has only been delayed, not banished. A similar tug-of-war is playing out between those who feel the U.S. dollar "should" decline in the years ahead and those who see the dollar strengthening significantly. Those who feel the dollar should decline look at the Federal Reserve's money-creation operations (buying $85 billion a month of mortgages and Treasury bonds) and see money expansion that devalues the existing base of dollars. Thus they feel the dollar "should" decline, and any rise in the dollar versus other currencies, oil and gold are temporary. Those on the other side are dollar bulls, of which I am one; I have consistently been presenting the case for a stronger dollar since early 2011. We see other dynamics in play that "should" push the dollar much, much higher. The technical case is encapsulated in this chart, courtesy of our Chartist Friend from Pittsburgh:

This is not to say that we don't believe expansion of base money is not dollar-negative; clearly, expanding money while the real economy of goods and services remains stagnant will gradually devalue the currency. But there are other forces at work that complicate the simple case for a dollar decline based on Fed money-creation. For example, money is constantly being destroyed as paid-in capital vanishes in writedowns and write-offs. Many readers insist money is not being destroyed, but it has to work both ways: money can't just be created, it can also be destroyed. To cite my previous example: if J.Q. Citizen bought a house in 2007 with $50,000 down payment in cash, and the house was sold in 2010 for less than its outstanding mortgage, that $50,000 is gone. It was real money, and it's gone. The fact that the purchase money went to the previous owner and mortgage-holder in 2007 does not mean the money is still floating around: a decline in asset valuations destroys money. Any loss booked by the bank is also real money, as the loss comes off the bank's cash reserve. So if the Fed prints $1 trillion and $2 trillion in losses are booked in the same time period, base money has actually declined. In effect, the Fed is creating money to offset the deflationary effects of deleveraging. There is another structural dynamic in play known as the Triffin dilemma or paradox. The basic idea is that when one nation's fiat currency is used as the world's reserve currency, the needs of the global trading community are different from the needs of domestic policy makers. Prior to 1971, the dollar was backed by gold, which acted as a supra-national anchor to the dollar's reserve status. The gold standard inhibited both massive trade deficits and money creation, so it was jettisoned.

The Triffin paradox is a theory that when a national currency also serves as an international reserve currency, there could be conflicts of interest between short-term domestic and long-term international economic objectives. This dilemma was first identified by Belgian-American economist Robert Triffin in the 1960s, who pointed out that the country whose currency foreign nations wish to hold (the global reserve currency) must be willing to supply the world with an extra supply of its currency to fulfill world demand for this 'reserve' currency (foreign exchange reserves) and thus cause a trade deficit. (emphasis added) Here is an informed exploration of the relationship between Gold And Triffin's Dilemma (Zero Hedge). A lively debate is taking place about how to "fix" the global currency so the U.S. doesn't have to run huge current-account deficits to provide liquidity and reserves for global trade. Some feel a return to the gold standard is the best solution, others favor a "basket of currencies" approach, while the International Monetary Fund (IMF) and other globalists unsurprisingly favor a supra-national new currency called the "bancor" overseen by (you guessed it) a global central bank. In my view, the euro currency is a regional experiment in the "bancor" model, where a supra-national currency supposedly eliminates Triffin's paradox. It has failed, partly (in my view) because supra-national currencies don't resolve Triffin's dilemma, they simply obfuscate it with sovereign credit imbalances that eventually moot the currency's ability to function as intended. What happens instead is the currency's central bank--in the case of the E.U., the European Central Bank (ECB)--attempts to square the circle by shifting surpluses from some nations (Germany) to those with structural imbalances via credit (debt). Correcting imbalances is the proper function of currencies, and the attempt to eliminate imbalances with a single currency has failed, for the simple reason you cannot eliminate imbalances between nation-states by brute force. Now the ECB is attempting to paper over the imbalances with bank-issued credit. But the problem with credit is that it accrues interest, which must be paid in cash by somebody. Issuing credit does not resolve imbalances, it simply transfers the imbalance from the currency ledger to the credit/debt ledger. Eventually the imbalances destabilize the system. That is what Europe is experiencing but refusing to admit. So where does the global recession leave the U.S. dollar? We know what happens in global recession: global trade declines as sales drop and "trade wars" arise to protect domestic economies from the ravages of global contraction. The global demand for U.S. trade deficits to create dollar reserves will thus also decline. Domestically focused observers think that the Fed is the only creator of dollars, but in effect the U.S. creates dollars--and must create dollars--when it buys more from other nations (imports) than it exports. To expand their own credit base, trading nations need more reserve currency. This is the heart of Triffin's insight. Another way of stating this is that the dollar will strengthen, buying more imports with fewer units of currency. Those who believe the Fed's expansion of its balance sheet will weaken the dollar are forgetting that from the point of view of the outside world, the Fed's actions are not so much expanding the supply of dollars as offsetting the contraction caused by deleveraging. Put another way, the global trading community and the domestic economy's interests align in a strengthening dollar. While many observers believe the Status Quo seeks a weaker dollar to boost exports, this overlooks the premium gained by the "exorbitant privileges" of the global reserve currency and petro-dollars. This premium is worth far more than marginal increases in exports. I have long held that the demand for oil will plummet on the margins as the global economy contracts. As the dollar strengthens, the U.S. will pay less for imported energy and earn more for exported energy. This decline in energy costs will ripple through the real economy, offsetting any decline in exports. A strengthening dollar lowers the cost basis of all goods and services originating in the U.S. A strengthening dollar also benefits trading nations, as the increasing value of their dollar reserves enlarges the base for their own credit. This is the irony of China's dumping of its dollar reserves: China only amassed such massive dollar reserves because it was running equally massive trade surpluses with the U.S. As the trade surplus shrinks, so too must China's dollar reserves contract. From the point of view of the currency markets ($2-$3 trillion traded daily) and global trading nations, the Fed's expansion of base money is marginal: after all, the U.S. has some $60 trillion in household assets, a $15 trillion economy, an expanding base of energy production, a dynamic private sector, a dominant military, the petro-dollar and the global reserve currency. As destructive as the Fed's policies are to the domestic U.S. economy, from this point of view the Fed's actions are stabilizing actions on the margin. The real action is in the global expansion/contraction of dollars from trade and in reserves. It boils down to supply and demand: the demand for dollars as reserves will remain high, while the supply will actually decline as global trade contracts. The dollar will rise in value for this reason alone. There is also the question of alternatives: what other currency could act as a reserve currency and trade in size without disrupting markets? The renminbi? It's not even convertible/liquid yet, and recall Triffin's primary point: countries like China and Japan that run trade surpluses cannot host reserve currencies, as that requires running large structural trade deficits. The euro? Good luck with a bet on papering over currency/trade imbalances with credit designed to drain the stronger economies of cash. The Swiss franc? It's now a proxy for the euro and it's simply too small to trade in size. Ditto all the other small currencies. Japan? With its history of trade surpluses and its demographic/fiscal cliff looming?

Not only are there no real-world alternatives to the dollar, its strengthening will benefit

everyone holding dollars everywhere in the world. That is a positive development.

Special offer exclusively for oftwominds.com readers: for two days only, Chartist Friend from Pittsburgh is offering a one-month trial subscription to his daily and weekly chart service for an extremely modest $5. Many of you have seen the Chartist Friend from Pittsburgh's insightful charts reprinted in my blog entries. In my view, his charts offer a unique value not found in other's charting systems.

As always, I receive no compensation from this offer.

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

(Kindle eBook $9.95) Read the Introduction (2,600 words) and Chapter One (7,600 words) for free.

We are like passengers on the Titanic ten minutes after its fatal encounter with the iceberg: though our financial system seems unsinkable, its reliance on debt and financialization has already doomed it.

If this recession strikes you as different from previous downturns, you might

be interested in my book

An Unconventional Guide to Investing in Troubled Times (print edition)

or

Kindle ebook format. You can read the ebook on any

computer, smart phone, iPad, etc. Click here for links to Kindle apps and Chapter One.

The solution in one word: Localism.

Of Two Minds Kindle edition: Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. What subscribers are saying about the Musings (Musings samples here): The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2012 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this essay to your site, or printed a copy for your own use.

Terms of Service:

|

Add oftwominds.com to your reader:

My Big Island Girl

Instrumentals by my friend

|

| Survival+ | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||