|

|

|

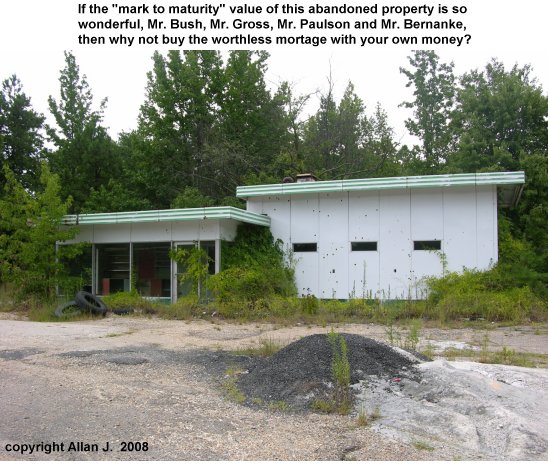

The Bush-Paulson-Bernanke Shock Doctrine Failed (September 30, 2008) Like many of you, I recently called my Mom to discuss protecting her nestegg of mutual funds and bonds. She commented that the entire hysteria and the supposedly pressing need to pass fascist legislation reminded her of The Shock Doctrine: The Rise of Disaster Capitalism I immediately concurred, for the Bush/Paulson/Bernanke "panic" and "plan" to hand unlimited funds and power without judicial or congressional oversight was ripped straight from the "Chicago School's" playbook of inducing a financial panic in developing nations and then moving in to "reform" the system into crony capitalism, a.k.a. corporate and political fascism joined at the hip--all covered with a veneer of propagandistic appeal to "restoring confidence in the market." As Klein carefully documents, the key elements in such a takeover are threats of financial collapse and a false urgency--both key drivers of the Paulson Plan. Lapdog Bernanke performed like any well-trained circus pup, mouthing absurdities, i.e. substantial benefits would flow to the taxpayers were we to grossly overpay for toxic assets held by insolvent banks. The meltdown is already underway, and handing control of trillions of dollars in taxpayer funds to a handful of insiders at Treasury will not stop that process. The phony urgency and Bailout would have transferred financialcontrol to a handful of Treasury cronies of Paulson; and while that wouldn't have stopped the meltdown--the price of decades of grossly obvious excesses--it would have enabled a relative handful of bankers and key players a "secret passage" to recovery of their fast-vanishing wealth--Paulson being Suspect One. As noted here before: told we had only hours til the Apocalypse on Thursday, Sept. 18, we find the world still working 12 days later. Look, trust has been destroyed by the institutions which are failing--the banks, the Treasury and the Fed. Bailing out the most worthless "assets" held by private lenders and investors will not restore trust. So global markets fall: rather than panic, we should say, bring it on. All sorts of "responsible" voices are calling for an end to mark-to-market accounting. The theory is that if we allow the banks to hold fictitious assets on their books for a few years, then eventually those assets will "regain value" and they can magically be sold for vast sums of money. Note to "responsible" pundits: the value of this property will not be higher two years hence, and neither will the mortgage, MBS or CDO based on it:

That was Japan's guiding principle in 1989, too--and how did that work for them? How about a 19-year long recession, briefly interrrupted by amemic growth resulting from global bubbles in credit and housing. This is all part of the insanely anti-market notion that "we like markets only when they go up." Here is how frequent contributor Harun I. put it this past weekend:

In his speech the other night, POTUS (President of the U.S.) warned that stocks might fall in value affecting retirement savings, house values may decline and jobs would be lost and banks would fail en masse. What he implied is that stocks can never go down again by more than a certain amount, and ditto for home values. Banks that make poor lending decisions must not be allowed to fail. In other words there can be no major downside to anything ever again without the taxpayer intervention. (Emphasis added: CHS) I would like to denounce this in some highbrow way but it needs to be called what it simply is: nuts.On a similar note, Frequent contributor U. Doran recommended this piece by Bill Fleckenstein: What's next, a ban on stock sales? Prices aren't to the government's liking, so it's changing the rules on the fly, and no one knows where or when new lines eventually will be drawn. I spent an extraordinary amount of time last week discussing the human responses to betrayal and loss of trust. The reason is simple: these are the bedrock of human interactions and transactions which, once destroyed, cannot be rebuilt except via a painstaking, arduous, patient process of trust incrementally being earned, not bestowed. The SEC's embrace of a ban on mark-to-market is based on an enormous fallacy: That letting banks keep fictitiously valued "assets" on their books for few years will magically enable them to make huge profits and re-capitalize via profits. As correspondent J.F.B. has often asked: how are banks going to make money as lending and credit tighten and a recession removes the need, desire and ability to borrow? It seems all too clear: they can't make money with distressed assets which are doomed to depreciate far further, and in a recessionary era of over-extended credit and consumers.

The answer is not to enable fantasy-based accounting and then hope that worthless assets

magically gain value: the answer is mark to market, and let buyers price the

distressed assets. Every firm which is insolvent should be allowed to go under; buyers

will appear at bankruptcy court auctions, and trust can be rebuilt, slowly

and in baby-steps, with new regulators, new enterprises and new players.

I have been mulling over the proposed bailout bill (which I have decided should be called the No Banker Left Behind Bill). I have the feeling that no matter what they do, something big this way is coming. I just dont know what form it will take. There Is Ultimately No Gaming the System: When the Micro Crash Reflects the Macro Crash (Zeus Y., September 29, 2008) The proposed 700 billion dollar bailout cannot really work from a system level. I know its real intention is to cover the butts of Wall Street investors, but you have the same problem in macro that homeowners have in micro. Nobody knows what homes are worth right now, so buyers are sitting it out. It isnt about restricted credit (even though that is a factor). It isnt about being too cash strapped to make a down payment (though that too is a factor). Its about not wanting to be suckered into buying something that may still be overpriced.

New Book Notes: My new "little book of big ideas," Weblogs & New Media: Marketing in Crisis

"Charles Hugh Smith's Weblogs & New Media: Marketing in Crisis is one of the most important business analyses I have ever read. It is the first to squarely face converging global crises from a business perspective: peak oil, climate change, resource depletion, and the junction of key social cycles will radically alter the business landscape in coming decades...."

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Ryan L. ($25), for your very generous contribution to this

site.

I am greatly honored by your support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||