|

|

|

||||||||||||

|

Fed to the Sharks, Part 1: The Fed Takes Our Money, Gives It to Banks Who Loan

It Back to Us at 16%

(April 8, 2014)

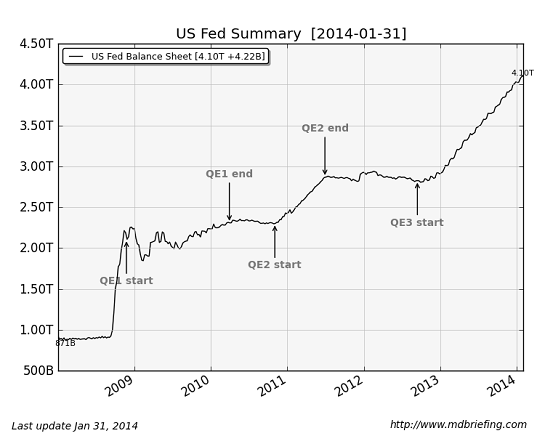

We're being Fed to the sharks, every day, one morsel at a time. What a way to go.... What can we say about the Federal Reserve's policies that hasn't been said a million times? How about simplifying the two primary purposes of Fed policies? I will cover one today and the second one tomorrow. Both involve feeding the 99.5% to the financier/ Wall Street/bank sharks. Longtime readers are familiar with Harun I.'s incisive analysis. Two of his recent commentaries can be found in Resolution #1: Let's Call Things What They Really Are in 2014 (January 15, 2014) and Doomed If We Do, Doomed If We Don't (February 12, 2014) In the above entries, Harun explained how the Fed's money creation has leveraged a global bubble in assets. At 72-to-1 leverage, the Fed's $3.3 trillion money expansion has generated inflation as well as asset bubbles, though the Fed and its cronies deny both asset bubbles and inflation.

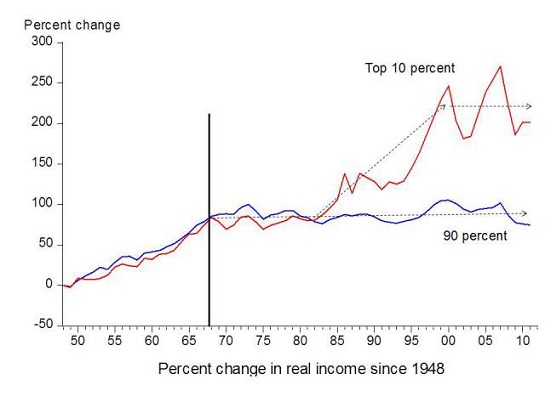

Inflation is the Fed's explicit, stated goal. The Fed wants prices to go up because that raises GDP (gross domestic product) and makes debt cheaper to service every year. But alas, real income isn't keeping pace--it's declining. Median household income is down 7% since 2000, but if we strip out the top 1% households, the decline for the bottom 99% would be more than 7%. And if we strip out the top 10% households, the decline of the bottom 90% of households is much more than 7%.

Household income for the bottom 90% has been stagnant for four decades:

So the Fed is robbing the purchasing power of our money as a matter of policy. In simple terms, the Fed is stealing purchasing power and delivering the stolen wealth to the financiers and banks, who borrow money from the Fed for near-zero rates of interest. And what do the banks do with the money the Fed stole from us? They loan it back to us at 16% (or more). Those of us who haven't just emerged from bankruptcy get offers from banks on a weekly basis: for transfers of credit card debt, new credit cards, cash advances, auto loans, home equity lines of credit, you name it. A recent offer from a Too Big to Fail bank offered a teaser rate of 0% for a few months, after which the credit card's interest rate reverted to 16%. This is how the Fed rebuilds the TBTF banks' insolvent balance sheets: it strips purchasing power from wage earners and savers and gives the banks free money which they loan to debt-serfs for somewhere between 5% and 24%, depending on the length of the loan and the collateral (or lack thereof). As Harun explained, the Fed steals our wealth, transfers it to the banks who then loan our money back to us at 16%. It almost makes you wish the Fed would just steal the money openly and give it to the banks and top .01% of financiers directly, without the sleight of hand of inflation and zero interest rate policy (ZIRP). The Fed implicitly claims (and many foolishly believe the propaganda) to be the ultimate financial power in the Universe:

If the Fed is so powerful, why is it so cowardly and fearful that it has to cloak its theft of our money and its transfer of the wealth to the banks? What's it so afraid of? That we might wake up to the fact that we're being Fed to the sharks, every day, one morsel at a time? Of related interest: The Federal Reserve's Nuclear Option: A One-Way Street to Oblivion (February 5, 2014)

Want to Reduce Income/Wealth Inequality? Abolish the Engine of Inequality,

the Federal Reserve

(January 28, 2014)

The Nearly Free University and The Emerging Economy: The Revolution in Higher Education Reconnecting higher education, livelihoods and the economy With the soaring cost of higher education, has the value a college degree been turned upside down? College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

The Nearly Free University and the Emerging Economy clearly describes the underlying dynamics at work - and, more importantly, lays out a new low-cost model for higher education: how digital technology is enabling a revolution in higher education that dramatically lowers costs while expanding the opportunities for students of all ages. The Nearly Free University and the Emerging Economy provides clarity and optimism in a period of the greatest change our educational systems and society have seen, and offers everyone the tools needed to prosper in the Emerging Economy. Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:  1. Debt and financialization

1. Debt and financialization

2. Crony capitalism 3. Diminishing returns 4. Centralization 5. Technological, financial and demographic changes in our economy Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA). We are not powerless. Once we accept responsibility, we become powerful. Read the Introduction/Table of Contents

Kindle: $9.95

print: $24

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

"You shine a bright and piercing light out into an ever-darkening world."

Subscribers ($5/mo) and those who have contributed $50 or more annually

(or made multiple contributions totalling $50 or more) receive

weekly exclusive Musings Reports via email ($50/year is about 96 cents a week).

Each weekly Musings Report offers five features:

At readers' request, there is also a $10/month option.

What subscribers are saying about the Musings

(Musings samples here):

The "unsubscribe" link is for when you find the usual drivel here

insufferable.

I am honored if you link to this essay, or print a copy for your own use.

Terms of Service:

|

Making your Amazon purchases through this Search Box helps support oftwominds.com at no cost to you:

Add oftwominds.com

|