|

|

|

||||||||

|

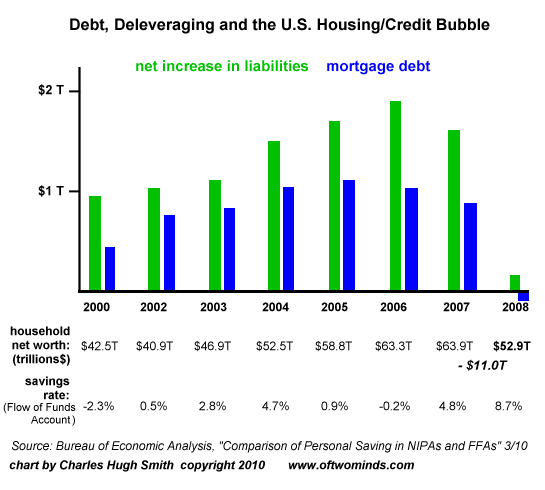

Seven Headwinds for the U.S. Economy (August 4, 2010) Even as the stock market rises on news both good and bad, seven trends offer strong headwinds to real growth in the U.S. economy. Of the many reasons for slow to negative growth ahead, I've chosen seven which are not amenable to easy manipulation or "fixes." 1. Small business has few incentives to hire and plenty of disincentives to trim payroll further. As I have often noted, any small business owner tempted to hire full-time workers must be suffering from a fit of temporary insanity: the last thing any business needs is higher overhead, more payroll taxes and all the costs imposed by "healthcare reform" a.k.a. "protect and empower the sickcare cartels." Meanwhile, The Wells Fargo/Gallup Small Business Index Hit a New Low in July, reflecting the "on the ground" perception by small business that the "recovery" is only tangible to those scoring fat contracts with the Federal government. Back in the real world of the private sector, the desert winds are blowing away the meager tumbleweeds left by the "stimulus," Federal Reserve manipulations (buying $1.2 trillion in mortgage securities, etc.) and propaganda (the stock market is rising, so that must mean the economy is prospering, etc.) 2. The U.S. money supply is not rising enough to fuel strong growth. It's almost counter-intuitive; how can the Federal government borrow and spend trillions of dollars, yet the supply of money in savings and checking accounts, money market funds and other liquid assets is barely growing? Hoisington Investment Management Company recently issued a report that showed how M2, the broadest measure of money in bank accounts, money market funds, etc. has grown by a meager 1.7% in the past year, the slowest growth in fifteen years. That reflects how little of the bailout and stimulus funds have actually ended up in the real economy. The correlation between slow growth in M2 and in the GDP is strong. 3. The job market is dominated by temp and free-lance/contract work. While temp jobs are rising at a strong 19%, year over year, private payrolls minus temp jobs is a negative .7%, meaning that permanent jobs in the private sector are still declining. I addressed the long-term forces which are transforming America into "free-lance nation" back in January of this year. 4. Financial insecurity is rising. American households are caught in a vise: even as wages stagnate and long-term unemployment erodes household incomes, the assets such as home equity which provided a cushion have also fallen. Medical and education costs are also rising, further squeezing households. As a result, the risk of "experiencing a major economic loss" is climbing. Those households which can save money have powerful reasons to sock away a cash cushion to weather possible emergencies such as job loss and medical out-of-pocket expenses, and few incentives to spend all their disposable income. The Pew Research Center recently issued a report, How the Great Recession Has Changed Life in America, which documents the new frugality and the punishing effects of the recession on household expectations, security and wealth. According to the report, median household wealth decreased by a whopping 19% from 2007 to 2009. Coupled with the poor job market, this has changed Americans' perceptions and planning. When asked to predict their financial behaviors once the economy recovers, 48% say they plan to save more, 31% say they plan to spend less and 30% say they plan to borrow less. All of those trends suggest there will be significantly less consumer spending in the years ahead--a sobering prospect in an economy which relies on houshold spending for much of its GDP. 5. The bedrock of middle-class wealth, the home, is still declining in value in much of the country. Sales have fallen, and outside of a few pockets driven higher by cash investor buying and shrinking inventories, the housing market remains weak. Foreclosures are still rising at a record pace, and the gap between what Americans lost in the housing bust and what they've recovered in value in the past year is in the trillions of dollars. 6. Households have gone from borrowing freely from their home equity to paying down debt. This process is called deleveraging, and this chart illustrates how equity extraction via mortgage refinancing has plummeted. The total amount Americans owe on their mortgages actually fell last year as households paid down debt.

The net result is American households no longer have the extra money to spend that they did in the heyday of the housing boom. Now they are devoting more money to reducing debt, which means there will be less money spent by consumers and thus less sales tax collected. 7. Taxes will rise, reducing household income and spending. While it appears that only the highest-income households will see a rise in their Federal tax rates as the Bush-era tax cuts expire, local and state taxes are on the rise, as are fees such as traffic fines which act just like taxes even if they avoid the dreaded label of "tax increase." In Philadelphia, property taxes are slated to rise a hefty 9.9%. Fairfield, New Jersey, passed an 11% increase in property taxes. These are not isolated incidents, but examples of a nationwide increase in local taxes. The legislature in Kansas recently raised the sales tax by 1% to 6.3%, a move which mirrors the widespread state and local rush to raise sales taxes across the board. Despite these large tax hikes, total revenues in many areas are flat or declining. Tax revenues in Nebraska are still falling, foiling forecasts, and Galveston County in Texas saw tax revenues fall by 17%. In addition to raising property and sales taxes, local governments are also jacking up parking rates, traffic fines and a multitude of other fees and levies. As I reported last October, some of the most outrageous examples are traffic tickets and related court costs. Given that all these substantial increases in taxes and fees have barely reversed the decline in local and state tax revenues, local authorities will undoubtedly press even harder for additional taxes to compensate for lower spending and housing valuations. This trend to ever-higher taxes and feed will have long-term negative consequences on household finances, local government revenues and consumer spending. It's called a positive feedback loop: the less households spend, the less taxes the local governments collect, causing them to raise taxes, which leaves households even less to spend, and so on.

Seven headwinds funneled together are not just a light breeze.

Of Two Minds is now available via Kindle: Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2010 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

Add oftwominds.com to your reader:

|

| Survival+ | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||