|

|

|

|||||||||||||

|

The Grand Failure of the Econometric Model (February 15, 2012) If the conventional econometric model based on metrics like forward price-earnings ratios and a declining unemployment rate is so accurate, then why did it fail so completely, totally and utterly in predicting the 2008 meltdown? A certain flavor of econometric model dominates conventional portfolio management and financial analysis. This model can be paraphrased thusly: seasonally adjusted economic data such as the unemployment rate and financially derived data such as forward earnings and price-earnings ratios are reliable guides to future economic growth and future stock prices. Here is an excellent example of econometric analysis, which (surprise!) concludes that the Dow Jones Industrial Average is headed for 15,000 as skepticism over economic growth and rising profits diminishes. Time to Reconsider the Upside for Stocks? As always, there are abundant charts presented to support the econometric call for steady growth in economic activity, corporate profits and stock indices. The same approach--that standard metrics of growth are not only accurate but they're all that's needed to accurately assess risk and gain--is on display here in the house organ of bullish bias, Barrons: Enter the Bull (Dow 15K or 17K). If this model is so accurate and reliable, why did it fail so completely in 2008 when a visibly imploding debt-bubble brought down the entire global economy and crashed stock valuations? Of the tens of thousands of fund managers and financial analysts who made their living off various iterations of this econometric model, how many correctly called the implosion in the economy and stock prices? How many articles in Barrons, BusinessWeek, The Economist or the Wall Street Journal correctly predicted the rollover of stocks and how low they would fall? Of the tens of thousands of managers and analysts, perhaps a few dozen got it right (and that is a guess--it may have been more like a handful). In any event, the number who got it right using any econometric model was statistical noise, i.e. random flecks of accuracy. The entire econometric model of relying on P-E ratios, forward earnings, the unemployment rate, etc. to predict future economic trends and future stock valuations was proven catastrophically inadequate. The problem is these models are detached from the actual drivers of growth and stock valuations. If you want to predict market action, the better model is to "follow the money" as Gordon Long does in Why Does The Market Keep Rising? (via U. Doran). This analysis is refreshingly cognizant of the fact that forward earnings, new unemployment claims and all the rest of the econometric spectrum are not predictive tools, they are merely perception management, i.e. justifications for current price action. Even worse, econometric models are all polishing the rear view mirror as a means of looking ahead, i.e. they are all based on the belief that recent action is a predictably accurate guide to what will happen next. This is another reason why the econometric models of forward earnings, unemployment rates and all the rest failed so utterly and completely: these metrics are incapable of predicting the next "credit event," "loss of risk appetite" or secular downturn. While the econometric models are all predicting renewed growth, rising corporate profits and an uptrend in job creation, consider this chart of the Ceridian Index. Does this chart reflect an expanding economy, or does it share all the traits of a contracting economy? (Chart courtesy of longtime correspondent B.C.)

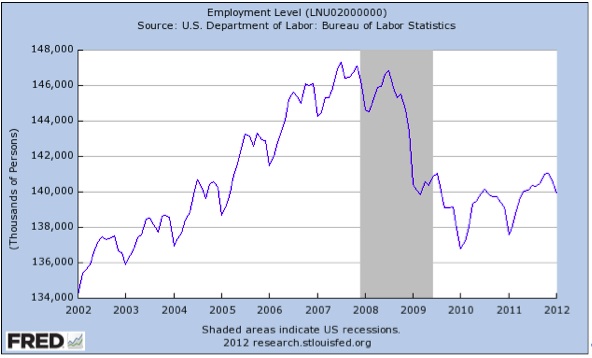

Indeed, an objective analysis (i.e. one not driven by the desperate need to paint a positive picture via propaganda and perception management) would find it obvious that the "real economy" rolled over in May of 2010, and that the market's recent ascent is nothing but Federal Reserve/central bank manipulation/intervention (see Gordon Long's analysis above for a full account of this dynamic). And what about energy consumption? (It's Not Just Gasoline Consumption That's Tanking, It's All Energy). And what about the vaunted employment resurgence? Where is it in this chart of actual employment, as opposed to unemployment rates, new claims, and other non-factors trumpeted by the cargo-cult witch doctors of econometrics as "proof of growth"?

Clearly, the number of people with actual jobs is declining, not rising. All manner of lipstick can be applied to the employment pig--weekly claims are dropping!, etc.--but the only number that actually matters is the number of people with jobs, and more narrowly, those with full-time jobs. In other words, laying off 10 million full-time workers and hiring back 10.1 million part-time workers with no benefits is a completely deceptive measure of employment income, as total compensation (wages and benefits) fell more or less in half and so did the income available for consumption and investment. Such a precipitous decline in income and resultant economic activity would be completely masked by a studiously coarse measure of employment. As for forward earnings--I have often described the dominant causal factor in the rise of U.S. corporate profits-- the decline of the U.S. dollar. In a nutshell, here's the story of rising profits: 40% of all U.S.-based corporate revenues are generated overseas, and a majority of profit increases result from these rising sales overseas. When these profits earned in euros, renminbi, yen, etc. are restated in U.S. dollars, then the profits magically rise. For example, 1 euro earned by a U.S.-based corporation in 2002 yielded about $1 when converted to dollars in the company's financial reports. In 2008, that 1 euro ballooned into $1.60 of profits due to the currency exchange rate of 1 euro=$1.60. Fully 35% of that profit was a result of dollar depreciation, not an actual increase in profit margins or goods and services produced. The Fed's campaign to destroy the nation's currency generated fabulous (and phantom) "growth" in corporate profits at the expense of every holder of the currency. Now that the U.S. dollar is in a secular uptrend, the Fed's shadow strategy to boost phantom corporate profits and thus the stock market is in trouble. Now all those phantom gains are threatening to vanish as the dollar strengthens. As I have noted many times, the vast majority of standard-issue financial pundits (SIFPs) are absolutely convinced that the Fed's $1 trillion expansion of its balance sheet will drive the dollar ever lower in the years ahead. I disagree, on a simple "follow the money" analysis: given that there is around $60 trillion in financial assets sloshing around an increasingly risky world seeking some sort of safe haven, the pressing goal of not losing what I have makes parking assets in U.S. dollar-denominated assets a risk-averse strategy. Recall that it's difficult to temporarily "park" a rather modest $1 trillion in, say, renminbi, bat guano or gold, because the entire global market for these assets is small or restricted (the RMB is not yet a floating currency that can be bought in virtually unlimited sums). For example, the gold market is around $8 trillion, of which 19% is held by central banks and 52% is in jewelry. It's difficult to locate $1 trillion of gold to buy. In contrast, it is comparatively straightforward to "park" $1 trillion in U.S.-denominated assets such as Treasury bonds, corporate bonds, stock funds, etc., and these assets have the additional benefit of being liquid, i.e. you can unload your position in relatively short order without destroying the global market for the asset. (Try that with bat guano or copper.) This need to park collateral-impaired financial assets in something that won't crater tomorrow or the next day is a powerful reason for some of that $60 trillion sloshing around to find a temporary home in dollar-denominated assets. Compared to the pool of digital money seeking safe haven, the Fed's $1 trillion expansion is simply not big enough to move global markets when the "risk-off" trade explodes.

Meanwhile, the cargo-culters gathered around the econometrics campfire are staring at the

glowing embers, entranced by forward P-Es of 14.6 and a 11K drop in new unemployment claims

(now 366,000, soon to be adjusted upward by 12K when nobody's looking) or

whatever runes painted on rocks they're looking at this week.

Of Two Minds Kindle edition: Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings, and an offer of a small token of my appreciation: a signed copy of a novel or Survival+ (either work admirably as doorstops). At readers' request, there is also a $10/month option. The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2011 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this essay to your site, or printed a copy for your own use. |

Add oftwominds.com to your reader:

My Big Island Girl

Instrumentals by my friend

|

| Survival+ | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||