Pensions Now Depend on Bubbles Never Popping (But All Bubbles Pop)

October 3, 2018

We're living in a fantasy, folks. Bubbles pop, period.

The nice thing about the "wealth" generated by bubbles is it's so easy: no need to earn wealth the hard way, by scrimping and saving capital and investing it wisely. Just sit back and let central bank stimulus push assets higher.

The problem with bubble "wealth" is it's like an addictive narcotic: now our entire pension system, public and private, is dependent on the current bubbles in stocks, real estate, junk bonds and other risk assets never popping.

But a funny thing eventually happens to financial bubbles: they all pop. And when the current bubbles pop, they will gut pension reserves, projections and promises.

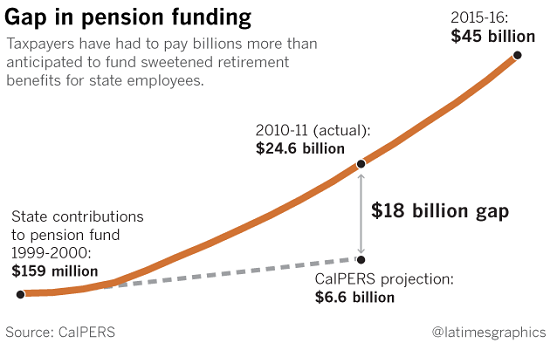

Take a look at the chart below of taxpayer contributions to Calpers, the California public pension fund. Note that in the heady days of Bubble #1, the dot-com era, enormous gains in Calpers' stock holdings meant taxpayers' contributions were a modest $159 million annually.

Based on bubbles never popping and monumental annual gains continuing forever, Calpers projected taxpayer contributions in 2010 of $6.6 billion. But since Bubble #2 had popped in 2008-09, stock market gains had cratered and as a consequence taxpayers had to pay almost four times the Calpers projection: $24.6 billion.

In a few short years, taxpayer contributions have nearly doubled, despite the outsized returns generated by Bubble #3, the largest of them all. By 2015, taxpayer contributions to Calpers totaled $45 billion, even as Calpers reaped huge gains in its stock portfolio.

So what happens to taxpayer contributions when all the asset bubbles pop? They go through the roof right when taxpayers are themselves facing staggering declines in their own personal wealth and the inevitable declines in income that accompany recessions. (What's a recession? I thought the Fed banned those.)

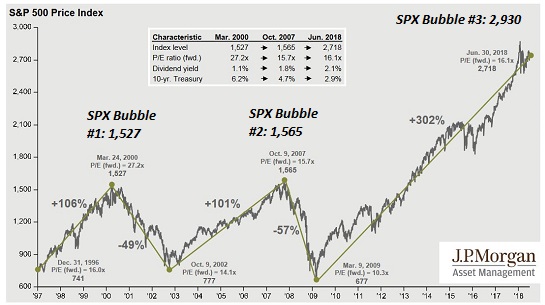

Here's a chart of the three stock market bubbles. Note the current bubble is the most extreme bubble.

Stock bubbles inflate on the euphoric belief that corporate profits will soar ever higher, forever and ever. But history suggests corporate profits tend to crash in global recessions and financial crises.

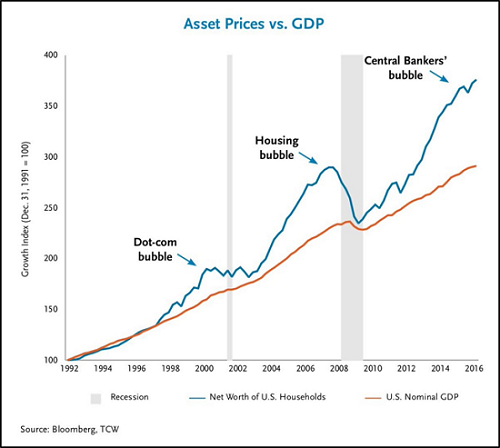

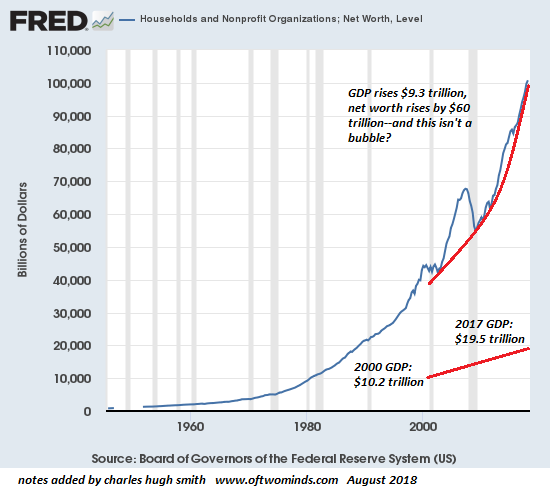

Meanwhile, household net worth and asset valuations have disconnected from the real world. GDP has risen modestly while assets have skyrocketed.

Private retirement assets (401Ks and IRAs) have bubbled higher, creating the temporary illusion of a "safe, secure" retirement because hey, past bubbles popped but the current bubble will never pop because the Fed won't let it pop.

We're living in a fantasy, folks. Bubbles pop, period. The Dow and SPX rose week after week and month after month in the 1999-2000 bubble, and again in the 2007 bubble, and so did junk bonds and housing. Everything rose in lockstep, lending support to the magical-thinking belief that this bubble will never pop because (insert excuse of the moment): housing never drops, the Fed has our back, etc.

Bubbles pop. To avoid this reality, commentators claim this is not a bubble.

Since it's not a bubble, it won't pop. But calling a bubble not-a-bubble doesn't mean

it's not a bubble. Wordplay doesn't change reality.

My new mystery

The Adventures of the Consulting Philosopher: The Disappearance of Drake

is a ridiculously affordable $1.29 (Kindle) or $8.95 (print);

read the first chapters

for free in PDF format.

My new book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition.

Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, VVV ($5/month), for your splendidly generous pledge to this site -- I am greatly honored by your support and readership. |

Thank you, Wojciech N. ($10/month), for your outrageously generous pledge to this site -- I am greatly honored by your steadfast support and readership. |

|